| Editor’s Note: Would you like to learn about water and other sustainable business investments on an on-going basis? Subscribe to SustainableBusiness.com’s specialized newsletter, Progressive Investor. |

By Ellen Pfeifer

Although currently overshadowed by the headlines from the Middle East and the War on Terrorism, the news about water is ominous. In Massachusetts, rainfall since Labor Day has been half the normal amount and rivers, streams and groundwater levels are extremely low. In Bourne, MA on Cape Cod, three of the six town wells have been closed and a fourth may soon follow as the result of ground water contamination by perchlorate from the nearby Massachusetts Military Reservation.

Fearing that public drinking supplies are potential targets for terrorists, some municipalities have been scrambling to take preventive action. Norwood, MA, for example, is considering the reactivation of a town well to serve as a backup to supplies from the Massachusetts Water Resources Authority.

The Environmental Protection Agency reported in April that the overall condition of U.S. coastal waters is fair to poor and that 44% of estuaries are “impaired for human use or aquatic life.”

In the United Kingdom, the Environmental Agency announced that estrogens in sewage effluent are adversely affecting the reproductive ability of male fish that live in freshwater lakes and streams.

And, at a recent environmental conference in Melbourne, Australia, a researcher projected a doubling of water demand over the next 50 years – even if the world’s population doesn’t increase.

Summing up all the concern, UN Secretary Kofi Annan warned on World Water Day (March 22), that “fierce national competition over water resources” could result in violent international conflict. “A looming crisis that overshadows nearly two thirds of the Earth’s population is drawing closer,” he said, “because of continued human mismanagement of water, population growth and changing weather patterns.”

Limited Supply, Poor Stewardship

Underlying these new stories are several stark facts: there is a finite supply of water, ever-increasing demand, and too much waste or pollution. Although three-quarters of the Earth’s surface is covered with water, only 3% is fresh and two-thirds of that is ice. Less than 1% is potable (safe to drink). Already 48% of the world’s population lacks access to drinking water, reports the Library of Congress’s Federal Research Division. According to UNESCO figures, the demand for water in the 20th Century increased six fold, more than double the rate of growth in the human population. Much of this increase was due to the dramatic expansion of irrigated land (agriculture now accounts for 70% of total water use).

At the same time, pollution in many regions further reduced the supply of water – sometimes with lethal consequences. For example, in India and Bangladesh, arsenic concentrations in potable water supplies are so high that millions of people are at risk of arsenic poisoning. “Water pollution, poor sanitation and water shortages will kill over 12 million people this year,” says Klaus Toepfer, of the United Nations Environment Programme.

Market Trends Driving Water Industry

In developed nations, at least, water has so far remained relatively cheap and readily available. However, the marketplace will undoubtedly begin to feel the impact of the increased pressures on water supply. And, as the multi-faceted water industry devises solutions to the problems, there may be significant opportunities for ecologically minded investors. According to Winslow analyst Namrita Kapur, these are some of the trends likely to shape the industry:

A Huge Market with Segments for Everyone

As of 1999, the water quality systems market in the US was approximately $86 billion. The largest segment is public wastewater (sewage systems) at 35% of the market or around $30 billion. Public water supply accounts for 34% or $29 billion ($24 billion accrues to municipalities and $5 billion to investor-owned regulated water utilities). Construction accounts for 11% of the market or about $9 billion. Services involve laying sewer pipe and pouring concrete. Equipment comprises 6% or about $5 billion and includes pumps, valves, meters, control and treatment systems. Treatment chemicals, bottled water, and point-of-use/point of entry systems each account for 4% of the market or about $3 billion. Contract operation and maintenance of both municipal and industrial water and wastewater treatment plants comprise the remaining 2% or less than $2 billion.

Of the total, private sector firms control only 31% of the market while regulated utilities make up 6% and municipalities comprise 63%.

A Wide Range of Water Companies

Broadly speaking, there are three advisable ways to invest in water industry stocks, according to analyst Kapur:

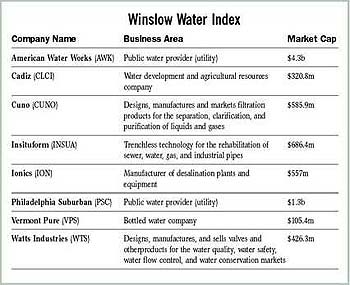

Water suppliers, that is, investor-owned utilities. The two biggest are American Water Works (AWK) and Philadelphia Suburban (PSC).

Companies that provide the technology for potable and ultra pure water. Ionics (ION) is the important player but smaller companies with good potential include Trojan Technologies (TUV.TO), Zenon Environmental (ZEN) and Cuno Inc (CUNO).

Small companies that have a distinct competitive advantage, a unique technology, or broad distribution that make them likely candidates for acquisition. Insituform (INSUA) has a patented process for “cured-in-place pipeline rehabilitation”. Watts Industries (WTS) is a leading manufacturer of valves. Vermont Pure Holdings (VPS) is the only pure play available in the bottled water industry and is the eighth largest US company in the segment (see accompanying article).

Finally, for one-stop shoppers, there is the 900-pound gorilla of the industry – Vivendi Environnement (VE). It comprises Vivendi Water, a waste treatment compan

y, plus several acquisitions including US Filter, Culligan, Everpure and Plymouth Products. From industrial cleanup to residential purification equipment to filters and bottled water, Vivendi covers the waterfront.

Featured Company

Vermont Pure Holdings: Taking the Waters Has Never Been so Profitable

By Channing Page

At the recent designer fashion shows in New York’s Bryant Park, liquid refreshment consisted of iced Evian and nothing else. On the sidewalks of Boston’s Back Bay, the young and fashionable can be seen sipping their Dasani as they dash to the next appointment. At board meetings around mahogany tables or brainstorming sessions in high tech cubicles, important discussions are washed down with water – in crystal glasses or straight from the bottle.

No longer just for quenching your thirst, water is chic. Water is cool. Water is a statement about the healthy lifestyle.

More and more Americans are turning to water as their beverage-of-choice. After decades of believing that things go better with Coke, the Pepsi generations have discovered the real Real Thing. But they aren’t simply turning on the tap. Instead they are reaching for those green or blue or ergonomically designed clear bottles containing their favorite brand, whether sparkling or still. They are gathering around the newly re-invented water cooler. And the soft drink companies have been quick to shape and exploit the trend. Indeed, the American bottled water market is the fastest growing segment of the beverage industry, having surged to a compounded annual increase of 10% over the past five years.

Vermont Pure: the one Pure Play

The brand names of the mass marketed waters evoke an image of remote bubbling springs, deep in the forest or the mountains, gushing a pellucid, icy cold elixir. Some of these brands may, indeed, have started as small, regional companies that bottled local spring waters. But, today, bestsellers like Poland Spring, Evian, and Aquafina are the products of the standard retail giants Perrier, the Danone Group, and Pepsi. There is only one publicly traded company that focuses exclusively on bottled water and offers investors a pure-play in this fast growing industry. That company is Vermont Pure Holdings (AMEX:VPS).

Headquartered in Randolph, VT, Vermont Pure started in 1990 as a small, local company, but its current size and reach are the result of a strategy of acquisition and consolidation. Having purchased or merged with other water companies, Vermont Pure now carries multiple brands: Vermont Pure, Iceberg Springs, Crystal Rock, and Hidden Spring.

Two Varieties, Two Markets

Despite the different names, the product line breaks down into two basic types of water: spring and filtered. Under labels including Vermont Pure Springs and Hidden Spring, the company sells spring water pumped from its properties in Randolph and Tinmouth, VT, as well as from a third-party property in Stockbridge, VT where it holds a 50-year contract. Permits regulated by Vermont law would allow the company to withdraw as much as 400 million gallons annually, but its current demand is projected to be only 4 million gallons.

Crystal Rock, the subsidiary that merged with Vermont Pure in October 2000, purifies and re-mineralizes ordinary tap water. It distributes the water in two, three and five gallon re-usable bottles to homes and offices. With a manufacturing plant located in Watertown, Connecticut, it can efficiently serve its primary customers in Connecticut and New York. But because it uses regular tap water, Crystal Rock could expand anywhere. For both sources, Vermont Pure’s bottled water reaches the consumer through two mechanisms. Single-serve bottles made of polyethylene terephthalate plastic (PET) are sold in retail establishments to individual customers. The larger jugs are delivered directly to individual and corporate clients. The former segment is growing faster, but it provides a lower profit margin. In the first quarter of 2002, Vermont Pure enjoyed a 22% increase in retail PET sales over the same quarter in 2001, and netted a 5% margin before taxes. By contrast, its Home and Office sales saw only a 3% increase, but achieved a 19% net margin before taxes. (Total sales of all products in this segment actually increased by 9%, but the gain was offset by a 9% decline in the sale of associated coffee services.)

A Pricey Acquisition

The merger of Vermont Pure and Crystal Rock was driven by the opportunity to expand the product line, to consolidate delivery routes, and combine back-office services. This coordination of internal operations has taken longer than originally expected, but is expected to drive cost savings in FY 2002 so that sales growth of 10-12% will be eclipsed by EBITDA growth of 15-20%.

However, these savings will come at a cost. In particular, the merger has added to Vermont Pure’s debt load. Certainly a strong cash flow will enable the company to pay down its debt schedule aggressively, but the current long-term debt- to- capital ratio of 52% will preclude any additional acquisitions in the near future.

Things Go Better with Vermont Pure?

Nonetheless, the company is poised for growth as part of an expanding industry. Many experts believe Vermont Pure will be acquired by one of the large retail companies. This scenario becomes more persuasive as companies find it increasingly difficult to secure sources of spring water. However, Howard Halpern of Taglich Brothers argues that Vermont Pure must reach a critical size of $100 million in revenue before a corporation of Coca Cola’s magnitude would consider such a step. And at a current level of $75 million in sales (as projected for 2002), it may take Vermont Pure three or more years to reach that point.

Water Table Down, Water Stocks Up

By Jackson W. Robinson

If there is any positive investment news to be extrapolated from the damage inflicted by global warming and changing weather patterns, one needs look no further than the water industry. Record setting temperatures and droughts are augmenting the already rising demand for clean water. As a result, water stocks are surging.

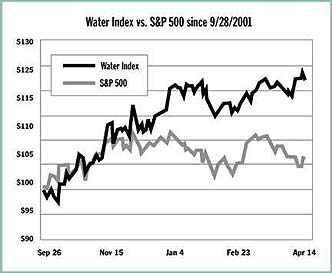

To measure the performance of the water stocks, we created the Winslow Water Index, an equally-weighted index of eight domestic water companies including two large utilities and a variety of related businesses including a small, independent bottled water firm, Vermont Pure Holdings.

Since the “bear market” hit bottom in the wake of 9-11, U. S. water stocks have out performed the overall stock market by a factor of three. Specifically, between September 28, 2001 and mid-April 2002, The Winslow Water Index is up +18% versus the S&P 500, which has gained a mere 5.8%.

The longer-term numbers for water stocks are also impressive. According to Debra Coy of Schwab Capital Markets, the Schwab water-stock index of 20 companies has outperformed all the major indices since it was created in 1999. Up +41% from inception, the Schwab index also includes two French and UK water companies.

Of course, drought is not necessarily good news for all water companies, especially water utilities that are forced to curb usage due to drought restrictions. Reduced unit sales means lower revenues and profits, at least until rate increases and/or alternative sources of water are secured. Certainly, the biggest boost to water utilities would be more rain, obviously a factor that is unpredictable.

In addition to water utilities, many other industries suffer because of drought. These include lawn and garde

n products, tourism, farming, car washes, developers, forestry, parks, and golf courses. From an investment point of view, companies in these industries that do not have secure water resources should be avoided.

As the demand for water becomes more acute, so will the demand for water filtration, treatment, recycling, and conservation products and services. We believe that the companies occupying these niches will continue to benefit from the drought, whether it is temporary or permanent. That translates into many attractive growth opportunities.

FROM Winslow Environmental News, a SustainableBusiness.com Content Partner.